First Time Insurance Buyer Guide: Steps to Get Started

Getting into insurance can feel overwhelming, especially if it’s your first time. Whether you need coverage for your home, health, or car, knowing the basics is key. This guide will help you understand the steps to choose the right insurance for you.

Key Takeaways

- Understand the different types of insurance and how they work to protect you and your assets.

- Learn how to assess your personal risk and coverage requirements to ensure you have the right protection.

- Discover strategies for comparing insurance providers and their offerings to find the best fit.

- Gain insight into the factors that influence insurance premiums and ways to lower your costs.

- Familiarize yourself with the insurance application process and the essential information required.

Understanding Basic Insurance Terminology and Concepts

Starting out with insurance can feel overwhelming. The insurance glossary and policy jargon are full of terms you might not know. But, it’s key to grasp the basics to choose the right coverage types and understand premium calculation. Let’s break down the basics and make insurance easier to understand.

Common Insurance Terms Explained

The world of insurance is filled with terms that might confuse you at first. Here are some key terms you’ll come across:

- Deductible – This is what you pay before your insurance starts covering costs.

- Copayment – It’s a fixed amount you pay for a service after your deductible is met.

- Policy Limit – This is the max your insurance will pay for a claim.

- Premium – This is the regular cost to keep your insurance active.

Different Types of Insurance Coverage

Insurance policies vary, each protecting against different risks. Here are some common coverage types:

- Health insurance – Covers medical costs like doctor visits and prescriptions.

- Auto insurance – Helps financially if you’re in a car accident.

- Homeowners insurance – Protects your home and belongings from damage or theft.

- Life insurance – Provides financial support to your family if you pass away.

How Insurance Premiums Work

The cost of your insurance policy, or premium calculation, depends on several factors. These include your age, where you live, how much coverage you want, and your risk level. Knowing how premiums are figured can help you choose better coverage and maybe even save money.

| Factor | Impact on Premium |

|---|---|

| Age | Older people usually pay more because they’re seen as higher risk. |

| Location | Places with more crime or natural disasters might have higher premiums. |

| Coverage Limits | More coverage means higher premiums. |

| Deductible | Lower deductibles mean higher premiums, while higher deductibles can lower them. |

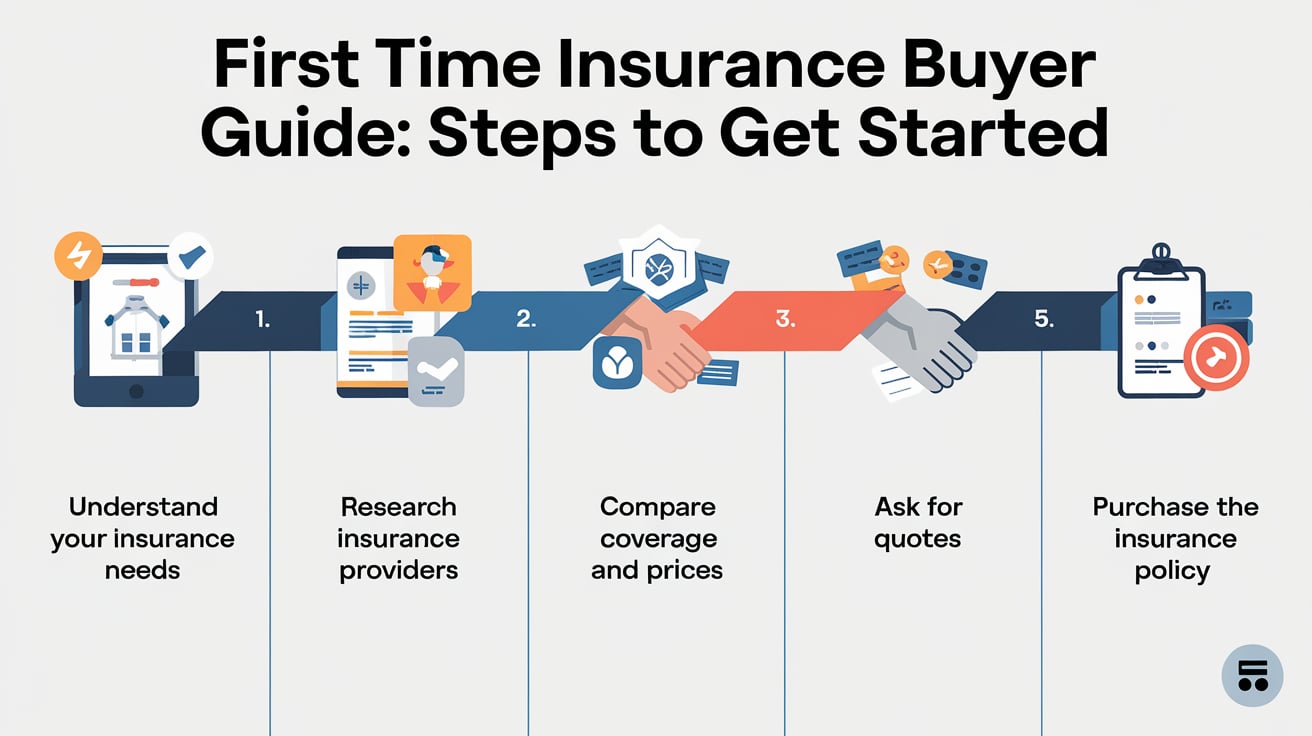

Your Step-by-Step Guide to Buying Insurance for the First Time

Buying insurance for the first time can feel overwhelming. But, with a clear plan, you can find the right coverage easily. This guide will help you through the insurance buying process, from policy selection to coverage evaluation.

- Start with Research: Look into the different types of insurance coverage like life, health, auto, and homeowner’s insurance. Learn what each type does and what you need.

- Assess Your Risks: Think about your personal and financial situation. Identify what risks you need to protect against. Consider your assets, debts, and lifestyle to choose the right coverage levels.

- Compare Providers and Policies: Compare what different insurance companies offer. Look at the policy details like coverage limits, deductibles, and what’s not covered. This helps you find the best deal.

- Understand the Quotes: When you get quotes, notice what affects premium calculations. Things like your age, where you live, and driving history matter. This helps you make a smart choice and maybe save money.

- Complete the Application: Get all the documents and info needed for your application. This includes personal details, work history, and financial info. Accurate info makes the insurance buying process smoother.

- Review the Policy: After approval, read your policy carefully. Make sure the coverage evaluation meets your needs. If not, make changes before you buy.

By following these steps, you’ll know how to buy insurance. Understanding policy selection and coverage evaluation is key. It ensures you get the financial protection you need.

Assessing Your Insurance Needs and Coverage Requirements

Finding the right insurance for you is key to protecting yourself and your stuff. It starts with a risk evaluation to spot potential dangers. Knowing your personal risk helps you choose the right insurance needs analysis and coverage estimation.

Personal Risk Assessment

First, think about your life now. Look at your job, family, and money situation. Your age, health, and any medical issues also matter. Think about risks like natural disasters, accidents, or lawsuits, based on where you live and how you live.

Asset Protection Strategies

Next, list your valuable things like your home, cars, and stuff you own. Figure out what they’re worth and how they’d be affected by bad events. Use insurance like homeowner’s, auto, or life insurance to protect your most important things.

Coverage Amount Calculations

With your risks and assets in mind, figure out how much coverage you need. This means thinking about the financial hit of bad events and how much protection you need. Think about your income, debts, and future money needs when setting coverage levels.

| Insurance Type | Recommended Coverage Amount | Factors to Consider |

|---|---|---|

| Life Insurance | 10-15 times your annual income | Dependent’s financial needs, outstanding debts, future expenses |

| Homeowner’s Insurance | Replacement cost of your home and belongings | Home value, contents value, liability exposure |

| Auto Insurance | Minimum state requirements, plus additional liability coverage | Vehicle value, driving record, risk of accidents |

By carefully looking at your risks, protecting your assets, and figuring out coverage, you can make sure your insurance is right. This gives you the protection and peace of mind you need.

Comparing Insurance Providers and Their Offerings

As a first-time insurance buyer, it’s key to compare insurance providers. Look at their policy features to find the best coverage for you. Check their financial stability, customer service, and policy options to make a smart choice.

When looking at insurance companies, check their financial strength and reputation. High ratings from A.M. Best or Standard & Poor’s show they can pay claims. Also, read customer satisfaction surveys and online reviews to see how they handle claims and service.

Look at the policy features and coverage each provider offers. Compare the limits, deductibles, and what’s not covered. Make sure the policy fits your needs. Key things to consider include:

- Coverage limits for liability, property damage, and medical expenses

- Deductible amounts and how they affect your premium

- Rider options for extra coverage, like roadside assistance or rental car reimbursement

| Insurance Provider | Financial Strength Rating | Customer Satisfaction Score | Policy Features |

|---|---|---|---|

| ABC Insurance | A+ | 4.8/5 | Comprehensive coverage, low deductibles, rental car reimbursement |

| XYZ Insurance | A- | 4.2/5 | Affordable premiums, customizable coverage, roadside assistance |

| Acme Insurance | A | 4.5/5 | High coverage limits, flexible deductibles, accident forgiveness |

By comparing insurance providers and their policies, you can find the right coverage for you. This research will help you make a smart choice as a first-time buyer.

Understanding Insurance Quotes and Premium Calculations

Insurance can seem overwhelming, but knowing what affects your quotes and premiums is key. Learning about insurance quote analysis helps you make smart choices. This can lead to lower insurance costs.

Factors Affecting Premium Rates

Many things can change how much you pay for insurance. Your age, where you live, your driving record, and credit score all matter. So does the type of coverage you want and how much you choose to cover.

Insurance companies look at these details to figure out how much risk you pose. Then, they set your premium.

Ways to Lower Your Insurance Costs

- Shop around and compare quotes from multiple insurers to find the best rates.

- Maintain a clean driving record and good credit history, as these can significantly impact your premiums.

- Consider raising your deductible, which can lower your monthly payments.

- Take advantage of any available discounts, such as those for safe driving, bundling policies, or being a loyal customer.

Reading and Understanding Quote Details

When you look at insurance quotes, it’s vital to understand what you’re seeing. Check the coverage limits, deductibles, and any extra fees or riders. This way, you can compare quotes effectively. Make sure you’re getting good value without losing necessary coverage.

| Factor | Impact on Premiums |

|---|---|

| Age | Younger drivers typically pay higher premiums due to increased risk. |

| Location | Rates can vary significantly based on the cost of living and claims history in your area. |

| Driving Record | Accidents, speeding tickets, and other violations can lead to higher premiums. |

| Credit Score | A higher credit score is generally associated with lower insurance rates. |

Knowing what affects your insurance quotes and premiums helps you manage costs. It also helps you find the right coverage for your needs. This knowledge is useful whether you’re new to insurance or looking to improve your current policy.

Essential Documents and Information for Insurance Applications

Getting into insurance can feel overwhelming, especially if you’re new. Knowing what paperwork and application requirements are key is important. Having your documents ready can make the application process easier and ensure you get the coverage you need.

Let’s look at what you’ll need for an insurance application:

- Personal Identification – You’ll need a driver’s license, passport, or ID from the government to prove who you are.

- Contact Information – Your address, phone number, and email are needed for communication during the application and policy management.

- Financial Details – You might need to share your income, assets, and debts for certain insurance types.

- Employment and Occupation – Your job and employer can affect your insurance rates and what you’re eligible for.

- Lifestyle and Health Information – For life, health, and disability insurance, you’ll need to share your medical history and current health status.

- Property Details – For homeowners or renters insurance, you’ll need to provide details about the property, like its address and age.

- Vehicle Information – For auto insurance, you’ll need to give information about the vehicle(s) you’re insuring, like the make and model.

Having these documents ready can make the application process smoother. Being prepared helps you navigate the insurance paperwork and requirements more efficiently.

By gathering the necessary information, you’re on your way to getting the right insurance coverage. This will help protect your assets and give you peace of mind.

Common Insurance Policy Exclusions and Limitations

Understanding policy exclusions and coverage limits is key in the insurance world. These details can greatly affect your coverage. Let’s explore what you need to know.

Standard Coverage Restrictions

Insurance policies often have standard exclusions. These may include natural disasters, acts of war, and intentional or illegal acts. It’s vital to review your policy to know these limits and plan well.

Optional Riders and Add-ons

To boost your coverage, think about getting additional insurance riders or endorsements. These can cover specific needs like identity theft or pet medical costs. They can also cover more of your personal property than the standard policy.

Policy Endorsements

Endorsements modify or add to your policy to fit your needs. They might increase liability limits, cover special items, or exclude certain risks. Check your policy to see which endorsements are available and how they can help you.

It’s important to know your insurance policy well. Review the fine print, look into optional riders and endorsements, and talk to your insurance provider. This way, you can tailor your policy for the best protection.

Tips for Choosing the Right Deductible Amount

When picking an insurance policy, choosing the deductible amount is key. The deductible is what you pay before your insurance starts. The right deductible affects your out-of-pocket costs and risk tolerance.

Here are some tips for picking the right deductible:

- Assess Your Financial Situation: Look at your savings, monthly budget, and if you can handle unexpected costs. A higher deductible might lower your premiums. But, make sure you can afford it if you need to file a claim.

- Evaluate Your Risk Tolerance: Think about how much risk you’re okay with. A lower deductible means more protection but costs more. Decide what’s more important to you: cost savings or financial security.

- Understand Coverage Levels: See how different deductibles change your coverage and benefits. A higher deductible might save you money but could limit your coverage or increase costs.

- Compare Quotes: Look at quotes from different insurers. Find the best mix of deductible, premium, and coverage that fits your budget and needs.

Choosing the right deductible is a personal choice. It depends on your finances, risk comfort, and coverage needs. By thinking about these, you can pick a policy that’s both affordable and protective.

“The right deductible can make all the difference in managing your insurance costs and coverage. It’s a decision that requires thoughtful analysis and planning.”

Understanding the Claims Process Before You Buy

Dealing with insurance claims can be tough, especially if it’s your first time. Knowing the steps can help you get ready and avoid problems later. We’ll look at how to file a claim, what documents you need, and how long it takes.

Claims Filing Procedures

First, you tell your insurance company about the issue. You can call, email, or use their website. You’ll share the details of what happened. Then, they’ll tell you what to do next, like filling out a claim form and providing documents.

Required Documentation

- Detailed description of the incident or loss

- Receipts, invoices, or other proof of ownership for any damaged or stolen items

- Photographs or video evidence of the damage or loss, if applicable

- Estimates or repair quotes from authorized service providers

- Copies of any police reports or other official documentation related to the claim

Timeline Expectations

The time it takes to process a claim varies. It depends on how complex the case is and how quickly everyone responds. Insurers usually reply within a few days after getting everything they need.

Then, they’ll look into it, check the details, and figure out how much to pay. This can take weeks or even months, based on the situation.

| Insurance Claims Process | Average Timeframe |

|---|---|

| Initial Claim Notification | 1-3 business days |

| Claim Investigation and Review | 2-6 weeks |

| Claim Payout | 1-4 weeks after approval |

Knowing about the claims process before you buy a policy helps. It prepares you for any future issues and makes sure your claim is handled well and quickly. Just remember to have all your documents ready to support your claim.

Working with Insurance Agents vs. Direct Insurers

When you buy insurance, you can choose to work with an agent or go straight to the provider. Each way has its own good points and downsides. The best choice depends on what you need and like.

The Benefits of Working with Insurance Brokers

- Personalized Guidance – Agents offer advice tailored to you. They help you understand insurance, ensuring you get the right coverage.

- Access to Multiple Providers – Agents work with many companies. This lets you compare rates and find the best deal.

- Claim Assistance – If you need to file a claim, your agent can guide you. They also speak up for you.

The Advantages of Buying Directly from Insurers

- Potentially Lower Premiums – Going straight to the provider might save you money. You avoid the agent’s fee.

- Increased Control – Directly with the insurer, you control your policy. You can customize it to fit your needs exactly.

- Convenience – Buying from the provider is often easier. You can manage your policy online or through an app.

Choosing between an insurance broker and a provider depends on your needs and preferences. Think about how much you know about insurance, how much you want to research, and how important personal advice and claim help are to you.

“The right insurance agent can be an invaluable asset, providing expertise and guidance to help you make informed decisions about your coverage. However, direct insurers offer the potential for cost savings and increased control over your policy.”

Conclusion

Starting your journey as a first-time insurance buyer? Remember the key insights from this guide. Learning insurance terms, figuring out what coverage you need, comparing providers, and handling claims are all important. These steps help you get the right policy for your situation.

Keeping up with policy management and coverage review is key. Your life can change, and so might your insurance needs. Work with your agent or insurer to update your policy. And don’t be afraid to ask for help with tough insurance choices.

Now you have the knowledge to make smart choices and protect your money. Understanding your insurance needs is an investment in your future. Congratulations on taking this big step towards a secure financial future!

FAQ

What is the difference between term life insurance and whole life insurance?

Term life insurance covers you for a set time. It’s cheaper but only pays out if you die during that time. Whole life insurance costs more but lasts forever. It also builds cash value over time.

How do I determine the right amount of life insurance coverage?

You should have 10-15 times your yearly income in coverage. This ensures your family is set if you pass away. Think about debts, future costs, and dependents when figuring out how much you need.

What is a deductible, and how does it affect my insurance premiums?

A deductible is what you pay before insurance kicks in. Higher deductibles mean lower premiums. But, make sure you can afford the deductible if you need to claim.

How can I save money on my car insurance premiums?

To save on car insurance, raise your deductible and use discounts. Bundling policies and shopping around can also help. Keeping a clean driving record is crucial for low premiums.

What is the difference between an HMO and a PPO health insurance plan?

HMOs are cheaper but limit you to in-network providers. PPOs let you see out-of-network doctors but cost more. Choose based on your health needs and budget.

How often should I review and update my insurance coverage?

Review your insurance every year or after big life changes. This keeps your coverage up to date with your current needs.

What is the difference between replacement cost and actual cash value coverage?

Replacement cost covers the full cost of a new item if yours is damaged or stolen. Actual cash value pays the current market value. Replacement cost is pricier but offers better protection.

How do I file an insurance claim, and what should I expect?

To file a claim, call your insurance, give details, and send needed documents. The company will then decide on your payout. Claims usually take a few weeks to settle.